The Branded Prescription Drug Fee (BPDF) is an annual tax created by the Patient Protection and Affordable Care Act to help fund the federal government’s expanded role in the US health care system. This annual fee is imposed on manufacturers/importers (covered entities) with aggregated branded prescription drug sales more than $5 million to specific government programs, which include Medicare Part D, Medicaid, Medicare Part B, VA, DoD, and TRICARE. The statutory fee to be invoiced and collected for 2025 is $2.8 billion.

Note December 31, 2025, the IRS issued a proposed regulation (REG-103430-24 2025-24153.pdf). As per the proposed regulation, “The proposed regulations update the existing regulations regarding the discounts, rebates, and other price concessions that CMS uses to determine branded prescription drug sales, to reflect changes made by the BBA and IRA and to reflect how covered entities are currently calculating their share of the fee. The proposed regulations add the Manufacturer Discount Program, which was established by the IRA, to the list of reductions that CMS uses to calculate branded prescription drug sales. The proposed regulations also update the percentage discount amount used for the Coverage Gap Discount Program to reflect the statutory change made by the BBA for plan years after plan year 2018.”…..This is still proposed and we will share thoughts once final. In the meantime, see below a summary and key dates relating to the current regulation.

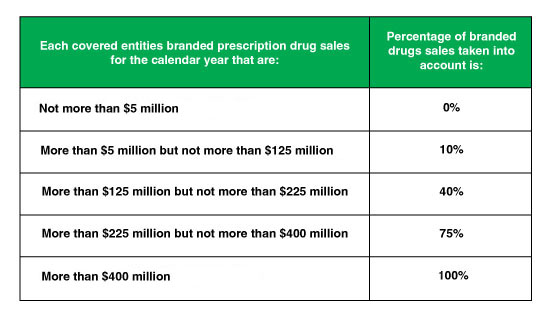

Each manufacturer/importer of brand products is responsible for a portion of the $2.8 billion statutory fee. As a reminder, below is a quick summary of how each manufacturer’s brand product sales to the government taken into account (i.e., numerator) is calculated. The denominator is simply the sum of all covered entities’ total brand sales to the government taken into account. The estimated fee will be based on the ratio (numerator/denominator) multiplied by the $2.8 billion, plus any adjustments (see IRS guidance for further details). The IRS invoice will show this calculation as well as the estimated sales by NDC by specified program. It’s important to note that the sales data in the 2026 fee year will be assessed based on 2024 sales.

Branded Prescription Drug Fee Tiers Based on Annual Sales

Figure. 1 – Annual BPDF Pharma Sales Tiers

Branded Prescription Drug Fee Deadlines and Key Dates for 2025

Click the link below for an illustrative example of the calculation and additional detail:

Key Dates and Considerations to Keep in Mind:

- No later than March 31: IRS Preliminary Fee Notice (letter 4657) mailed

- March 1 – May 15: Opportunity to evaluate and dispute preliminary IRS fee

- No later than August 31: Final Invoice (letter 4658) mailed (including dispute resolution, if applicable)

- No later than September 30: Final fee due

- November 1: Submit form 8947 (note this is an optional form)

Considerations

We recommend the following to ensure your organization is accruing and paying the appropriate amount: :

- Consider developing a process and tools to support the branded drug fee analysis.

- Estimate your sales and forecast for each applicable government program and estimate your share of the annual aggregate BPDF.

- Monitor and update your estimate as actual data becomes available and true up as needed.

- Review your IRS Preliminary Fee Notice to confirm that the IRS sales and estimated fee information appear accurate or reasonable based on your estimates.

- Monitor your data related to specified government programs on an ongoing basis to confirm that the data is accurate.

- If you have an orphan drug and would like to remain in the orphan drug exclusion rules, confirm that you meet the exclusion criteria. Note this exclusion is eliminated if the orphan drug is approved for any non-orphan indication.

- Evaluate whether it is beneficial to voluntarily file form 8947. While the form is not required, timely filing may help confirm the company’s Medicaid Supplemental Rebates and that orphan drug designations are accurately reflected in the BPDF invoice for the IRS.

We understand these activities can be challenging due to factors such as limited program knowledge, compressed timelines, limited team bandwidth, and complexity. Here is how we can help:

BPDF Analysis and Finance/Accounting Accrual Support:

- Prepare tools and advice to help estimate your BPDF and accrue appropriately.

- Provide advice and/or assistance necessary for proactively monitoring data and avoid future disputes.

- Assist with developing or enhancing your BPDF accrual process and or tools.

- Develop or enhance BPDF process documentation (e.g., Standard Operating Procedures).

- Provide BPDF trainings and or develop training materials.

- Provide guidance to navigate the BPDF process.

- Provide guidance to complete IRS Form 8947 and assist with submission.

References:

- Federal Register Vol. 79

- Annual Fee on Branded Prescription Drug Manufacturers and Importers

- Statuary Updates to Branded Prescription Drug Fee Regulations

For more information and how IntegriChain can assist your organization, contact nlynch@integrichain.com.

CONTACT US FOR MORE BPDF TAX INSIGHTS

About the Author

Nick Lynch

Nick Lynch is a Partner at IntegriChain and is based in the Philadelphia area. He is experienced in providing Contracting Strategy, Gross to Net, Commercial and Government Pricing compliance, and Fair Market Value support with a focus on operational, strategic, regulatory, and financial risks for emerging small, mid‐size, and top‐ten pharmaceutical and biotechnology companies.

About the Author

Ryan McGovern

Ryan McGovern is a Senior Manager, Advisory Services, and is experienced in providing Commercial Contracting & Validation Strategy, Formulary & Medical Policy Review, Medicaid Processing & Validation Strategy, Drug Price Transparency Strategy, and Customized Analytics for emerging small, mid-size, and top-ten pharmaceutical and biotechnology companies. Prior to FCS, Ryan led the Analytics and Reporting practice at IQVIA, where he developed a wide range of customized Analytics surrounding Commercial, Medicaid, Coverage Gap, Government Pricing, and GTN areas. Ryan has also led Commercial and Medicaid Operational practices over the last 20 years. Ryan is an integral part of the onboarding process across Commercial and Medicaid lines of business. He ensures Commercial contract language supports robust validations, resulting in optimal exclusion savings. Ryan also collaborates with manufacturers to deliver customized analytics solutions.